While most of the West is drowning in debt, governments worldwide are running huge deficits, and politicians are actively targeting your retirement savings for new taxes…

There is one country in South America with one of the most resilient pension systems on the planet and a debt-to-GDP ratio that would make a Swiss banker exceptionally jealous.

However, I am not here to sell you a dream, and some critical things have also changed for the worse in Chile.

Crime is no longer a distant concern, as it has increased noticeably lately.

Furthermore, their local Spanish is quite hard to understand, even for fluent speakers like myself.

Nevertheless, the everyday pros of living there are absolutely massive.

I lived there, and I still firmly consider Chile one of the best places I have ever lived, but…

Is it still worth moving to Chile in 2026?

Is the “Prussia of South America” still the unquestionable gold standard for expats in the region? As a South American myself, I am closely watching how the entire continent is shifting structurally in 2026.

I am considering writing similar articles on other South American countries too, so tell me in the comments which country you would like me to cover next.

For Chile, we are starting with a major red-flag factor that most expat writers are simply too afraid to mention.

Safety and the Urban Crime Shift

Until 12 years ago, Chile was proudly ranked as the 3rd safest country in all of Latin America. Expats constantly boasted about walking home safely at midnight in Santiago, but that pristine reputation is cracking.

A mega-gang called Tren de Aragua moved in from Venezuela and aggressively established a presence across all regions of Chile. Police operations targeted the core cells, but fragmentation created something arguably worse through autonomous subgroups operating with more violence and far less predictability. Kidnapping and extortion cases jumped significantly as a result.

The 2024 kidnapping and murder of former Venezuelan officer Ronald Ojeda Moreno in Santiago dominated national headlines and shifted public perception overnight. Chile’s homicide rate currently stands at 6 per 100,000. That is much lower than Ecuador at 46 per 100,000, and still better than most of the region.

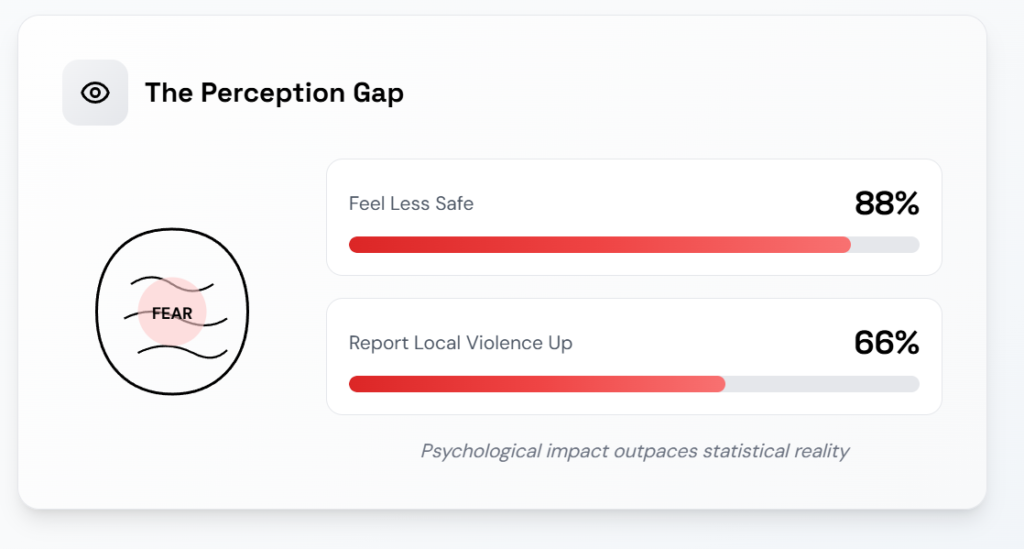

But perception moved much faster than the actual statistics.

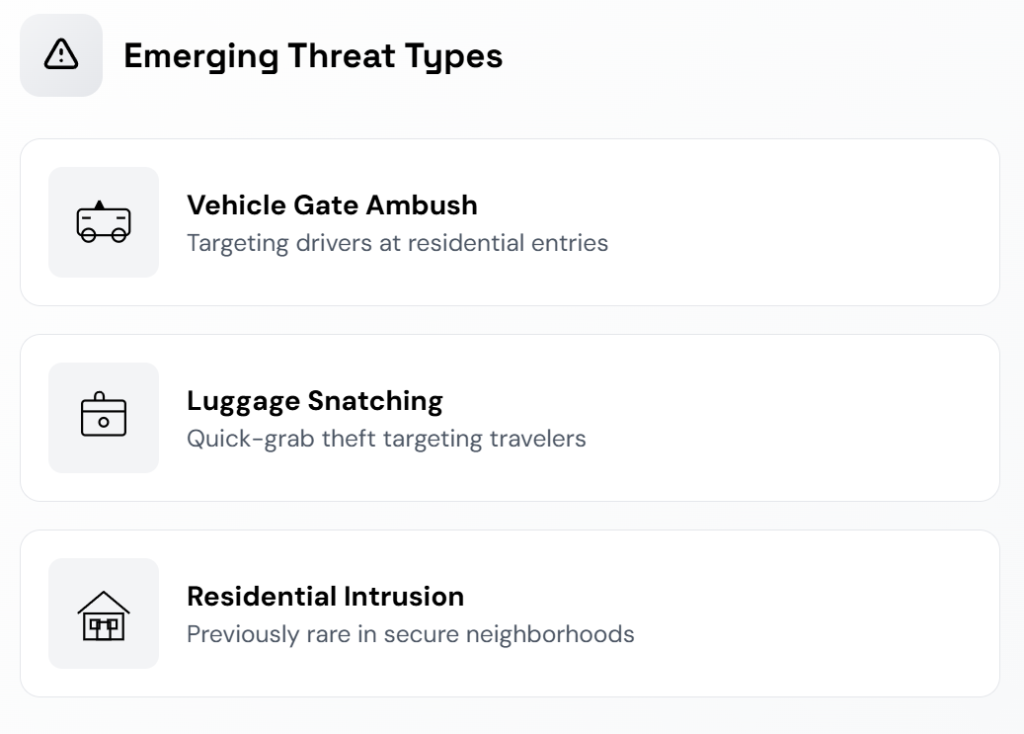

Nearly 88% of the population now feels crime has worsened, and two-thirds report increased violence directly in their own neighborhoods. Portonazos, or carjackings, became common enough to earn a household name across the country. Residential home invasions increased, and maletazos targeting tourists’ luggage added yet another layer of required caution.

Expats who moved to Chile in 2018 describe a distinctly different country than those arriving in 2026.

Some specific types of crime soared at a truly alarming rate.

Between 2018 and 2020, Chile averaged around 350 kidnappings per year. In 2024, that shocking number hit 868. Organized crime-linked incidents reached 775 per 100,000 in 2024, alongside continuous year-over-year increases in arms trafficking prosecutions.

Do not get me wrong; Santiago is not Caracas or Rio de Janeiro, and the inherent danger is nowhere near those extreme levels. Chile remains safer than 80% of Latin America, but the safety gap has narrowed and the premium has eroded.

Still, outside major cities like Santiago or Valparaiso, you can find incredibly safe and peaceful neighborhoods. Conversely, metropolitan areas like Puente Alto, which some locals sarcastically dub “Puente Assalto,” require much more everyday caution.

The next issue does not just require caution, as it aggressively hits your wallet every single day. Before revealing it, I would like to ask a small favor: if you enjoy this episode, please hit the like and subscribe buttons.

The Price Tag

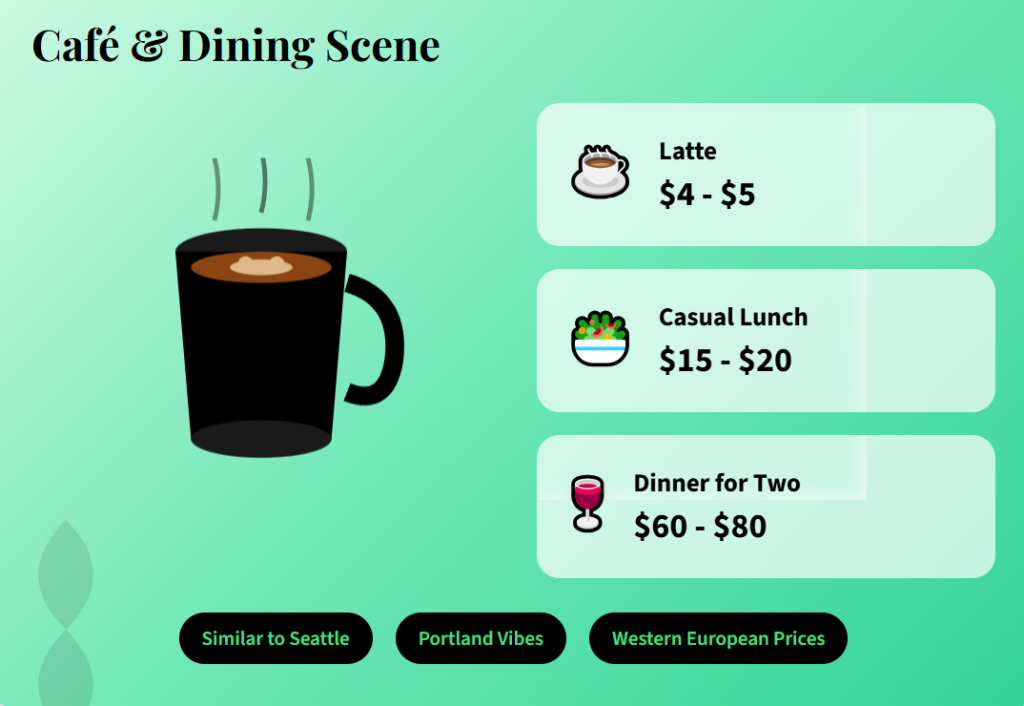

Chile is currently the second most expensive country in all of South America. Some common grocery items in Santiago cost more than in major American cities, like Cleveland, Ohio. High logistics costs and Chile’s relative geographical isolation relentlessly push prices up across the board.

Imported goods carry steep tariffs that make them even more expensive on the shelves. Even local produce runs more expensive than in neighboring countries because Chile’s wages and operational standards far exceed the regional average.

Dining out in premium areas like Las Condes or Vitacura rapidly approaches Western European pricing. A mid-range dinner for two with wine easily hits $60 to $80. Coffee shop culture mirrors Seattle or Portland rather than Lima or Quito, with a standard latte costing $4 to $5.

A casual lunch out will cost you around $20 per person.

This psychological mismatch severely disappoints some people who hear “South America” and automatically expect 50% savings. You generally get 10% to 15% savings compared to the US. You might achieve 20% savings if you live exactly like a local and strictly avoid expat neighborhoods.

Monthly budget estimates for 2025 and 2026 place a single person at around $1,400. A family of four needs approximately $2,400 to live comfortably. These figures firmly place Chile above Brazil, Argentina, or Peru in terms of cost.

Only one country in South America costs more than Chile right now. I recently ranked the cost of living for every country in South America.

The widespread fantasy of stretching a $3,000 pension into a luxury lifestyle evaporates when rent, food, and basic utilities easily consume $2,200. The financial margin for travel, dining out, and unexpected expenses shrinks down to $800 per month. Therefore, Chile is absolutely not a budget destination.

It is a destination designed for those who actively prioritize quality of life over rock-bottom prices. The roads work perfectly, the water is clean, the garbage gets collected on time, and the power reliably stays on.

If overall cost is your only filter, Peru or Ecuador will easily win. If cost-per-unit-of-stability is your primary filter, Chile suddenly starts to make perfect sense. While prices are easy to measure on a spreadsheet, there is also a much more intangible obstacle to conquer.

The Language Barrier

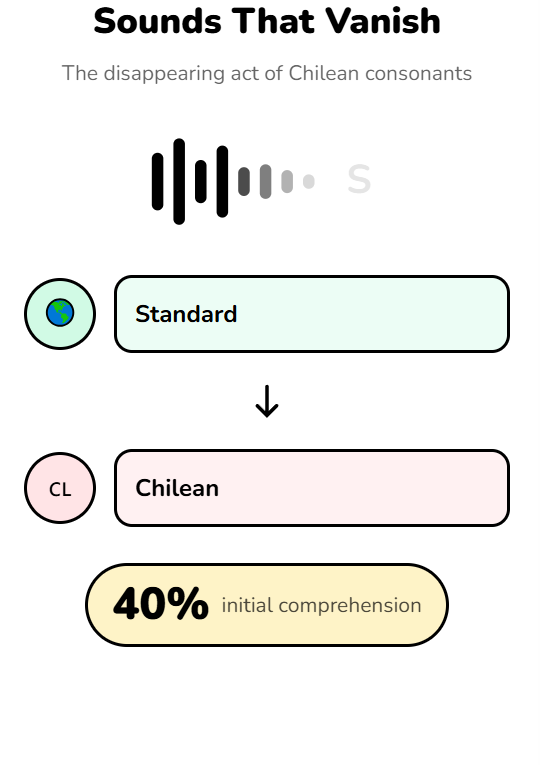

Sometimes, even highly fluent Spanish speakers heavily struggle upon arriving in Chile. I originally learned Argentinian Spanish, and I arrived in Santiago feeling incredibly confident. Then, a local from Quinta Normal asked me a simple question, and I caught maybe 40% of the words.

Chileans notoriously drop final consonants at the end of words, and the ‘s’ sound frequently disappears completely. For example, “¿Cómo estás?” casually becomes “¿Cómo estai?” They constantly inject chilenismos, which are rapid colloquial terms entirely unique to Chile, into every single sentence.

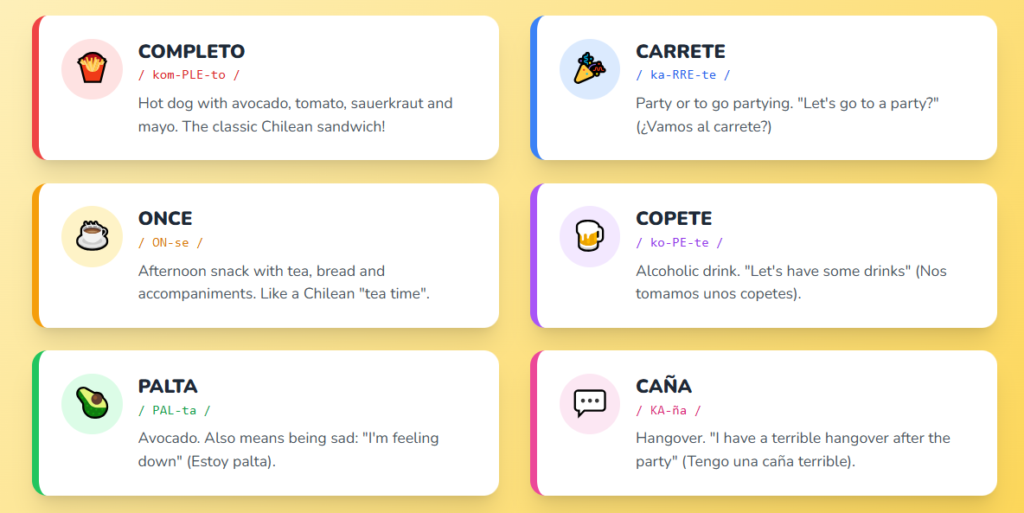

The word ‘cachai’ appears in roughly every third sentence, as it universally replaces ‘entender’ in normal daily conversation. A pololo is a boyfriend, while a polola is a girlfriend. Furthermore, “al tiro” means right away, a carrete is a party, a copete is an alcoholic drink, and palta is the beloved avocado they put on absolutely everything.

If you learned standard variations of Spanish, all of this vocabulary will sound completely alien to you.

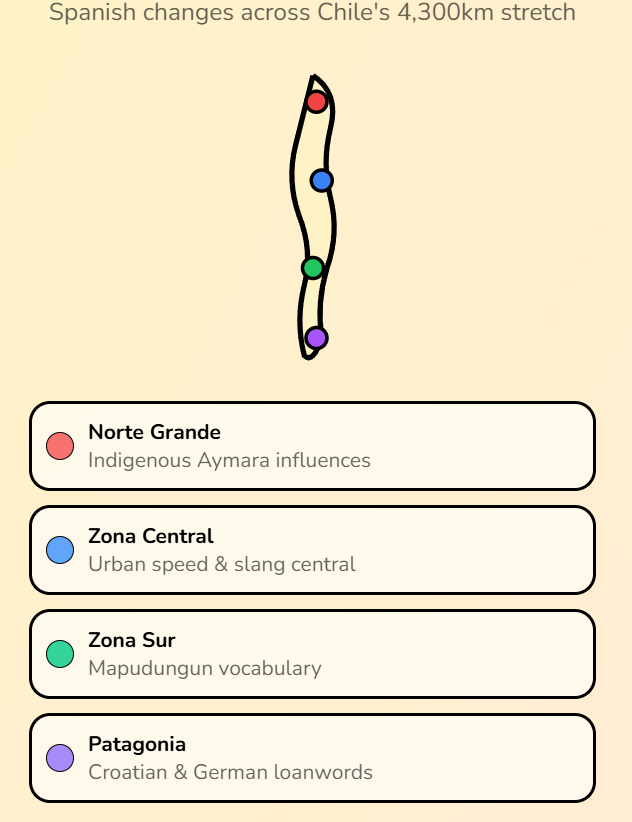

There is a massive amount of non-Spanish linguistic influence, ranging from indigenous Mapudungun and Quechua to various European languages. The ubiquitous word ‘cachai’, for example, actually originates from the French verb “cachar,” meaning to understand.

If you are not used to Chile, you will probably need at least six months of deep immersion just to grasp everything, especially the fast spoken Spanish. The initial learning curve is significantly steeper than in any other Latin American country. You will realistically spend months catching fragments of conversations and desperately piecing together context from body language and vocal tone.

Imagine walking into a bustling café and ordering a simple coffee. The barista asks a standard question, and you just nod and smile because you understood the first two words and none of the rest.

You enthusiastically meet locals at a social event, and they politely speak to you slowly at first, but then they forget and rapidly revert to normal speed. You will spend your entire first year nodding much more than you ever expected to. And remember, I am talking only about Santiago, which was the specific place where I lived.

Since Chile is a massive country geographically, there is also plenty of complex regional variation to navigate. If you can tolerate a longer adjustment period and strategically lean on English-speaking expat networks during your first months, this becomes entirely manageable. Now comes the specific part that makes long-term life significantly easier in Chile.

Pro Number 1: The Pension Revolution (or Why Chile Won’t Go Bankrupt)

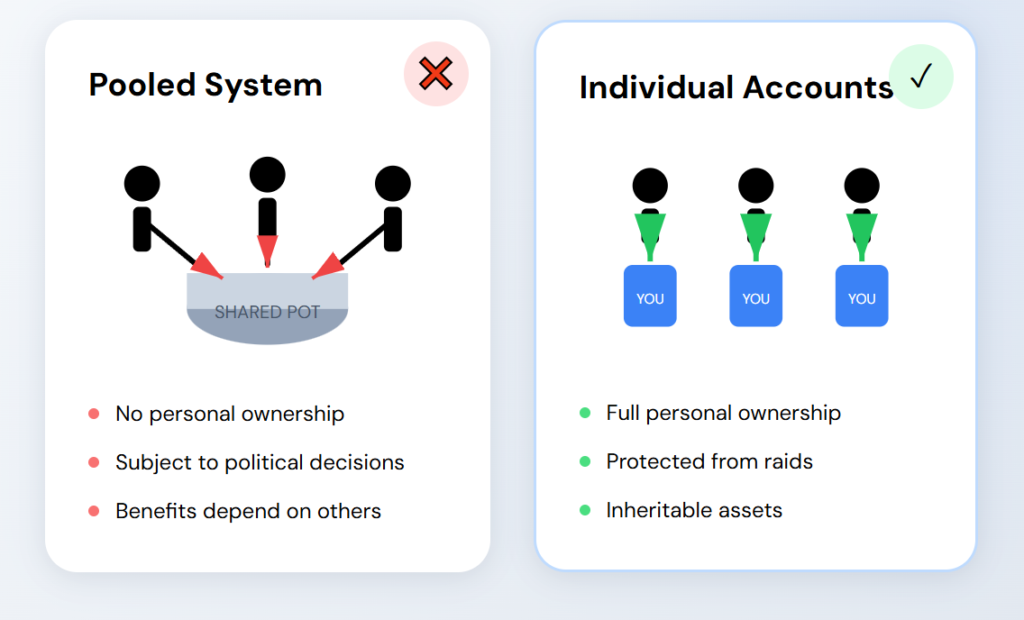

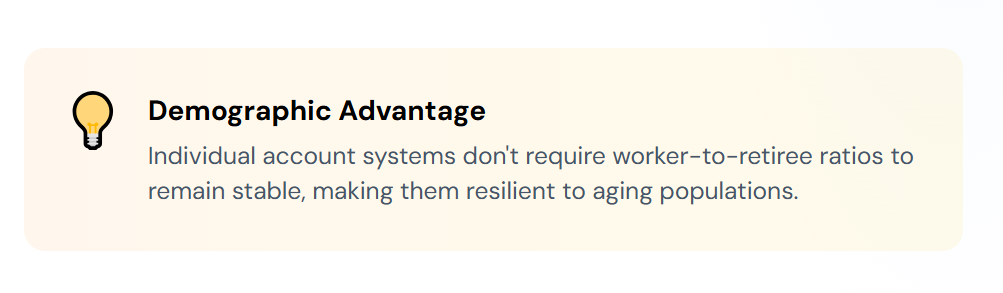

Most Western countries currently face an unprecedented and terrifying pension crisis. In the U.S. and most of Europe, Social Security runs a deeply flawed pay-as-you-go model where current workers directly fund current retirees. As national populations age and birth rates severely drop, the math collapses and debt snowballs out of control.

The core ratio of active workers to retirees simply becomes entirely unsustainable over time. Politicians are forced to either raid existing pension funds or dramatically raise taxes to cover the glaring shortfalls. The entire system fundamentally depends on perpetual population growth that is absolutely no longer happening.

Chile brilliantly solved this issue 40 years ago when they bravely took a radically different path in the 1980s. A brilliant group of Chilean economists trained at the University of Chicago under Milton Friedman returned to Chile and firmly convinced the government to scrap the broken old system. They effectively created the AFP model, which stands for Administradoras de Fondos de Pensiones.

Individual capitalization successfully replaced the doomed pay-as-you-go structure forever.

Each worker now contributes to a secure personal account, and the AFP system actively operates through competitive private pension fund administrators. You have the freedom to choose your specific AFP and your exact desired risk level. Your hard-earned money gets invested directly into stocks, bonds, and other productive physical assets.

The account belongs entirely to you, meaning that when you retire, you safely withdraw from your own personal funds. Corrupt politicians cannot legally raid it to arbitrarily pay for current government expenses. Your retirement pension depends strictly on what you personally contributed plus your investment returns, avoiding dangerous government IOUs and empty promises that might default when demographics inevitably shift.

Chile’s pension funds smartly hold real assets, including toll roads, active factories, massive buildings, and solid equity in successful corporations. This represents highly productive capital that remains firmly inside Chile, directly funding vital national infrastructure. Compare this to the U.S., where Social Security simply holds government bonds backed entirely by future tax revenue that may never actually materialize.

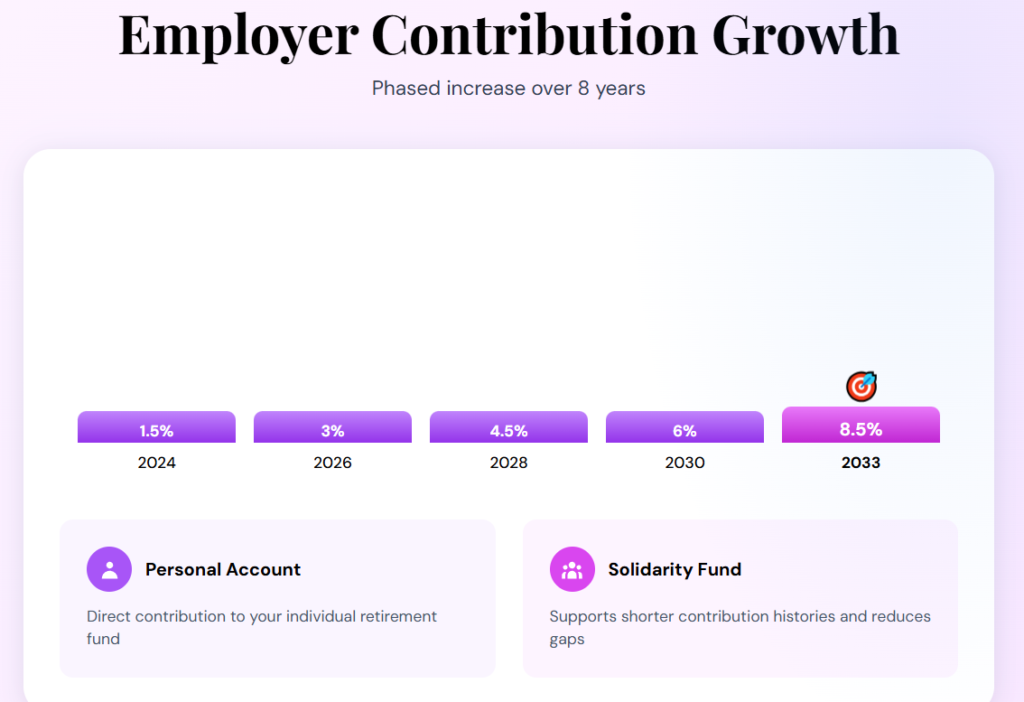

The comprehensive 2025 pension reform smartly added a mixed layer through Law 21.735. Mandatory employer contributions now steadily increase from 1.5% to a target of 8.5% by the year 2033. Furthermore, innovative Generational Funds actively shift your risk profile automatically as you physically age.

Workers in their 30s naturally get much more aggressive equity exposure for growth. Conversely, workers in their 60s safely move their wealth to highly conservative bonds. Ultimately, Chile does not face the terrifying pension fund time bomb currently threatening Europe, Japan, and North America due to plunging birth rates.

The system is certainly not perfect, but it is structurally far sounder than those of most OECD countries. If you lose sleep worrying about governments raiding retirement accounts or inflating away your life savings, Chile offers a proven model that does not rely on demographic miracles. That impressive fiscal discipline actively extends to exactly how Chile treats your personal income when you first arrive.

Pro Number 2 – The Tax Holiday: Three Years of Breathing Room

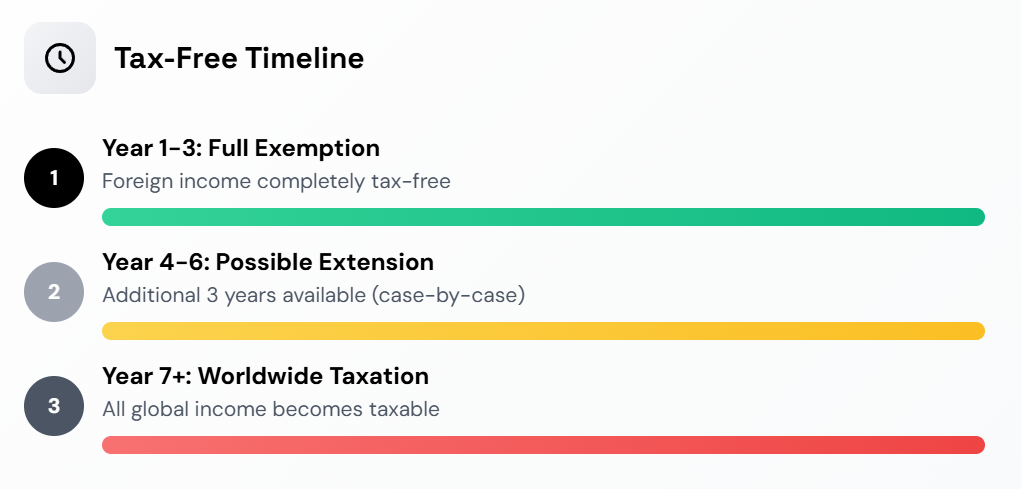

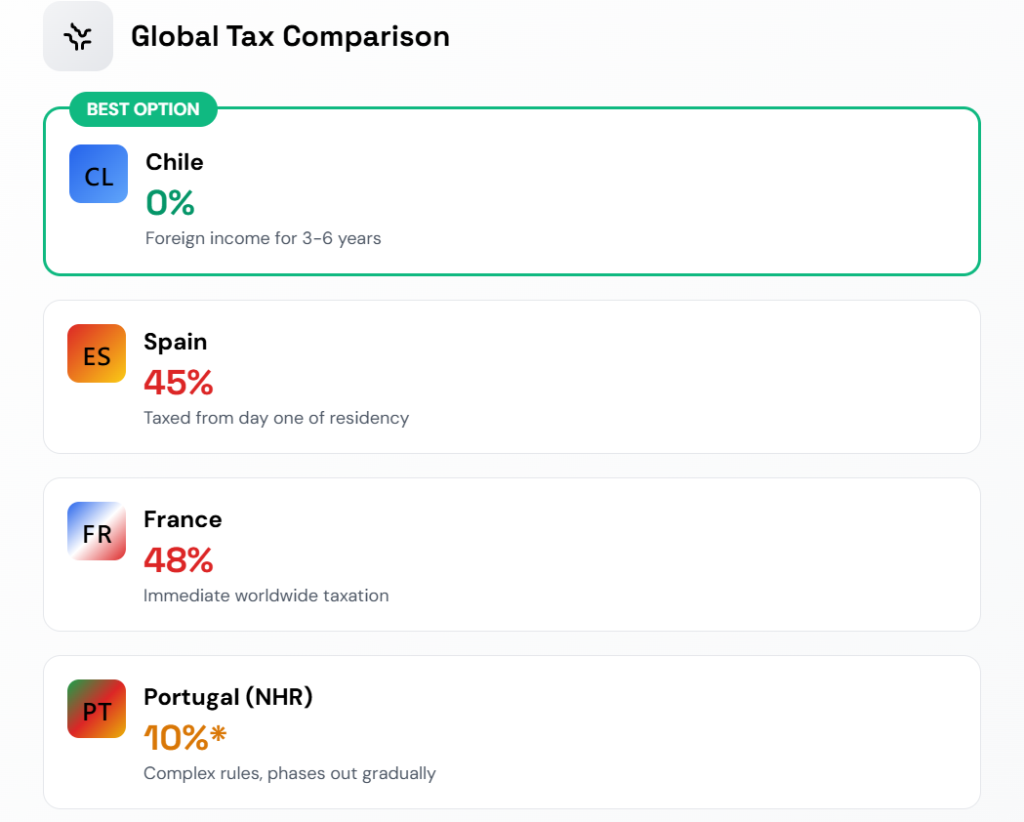

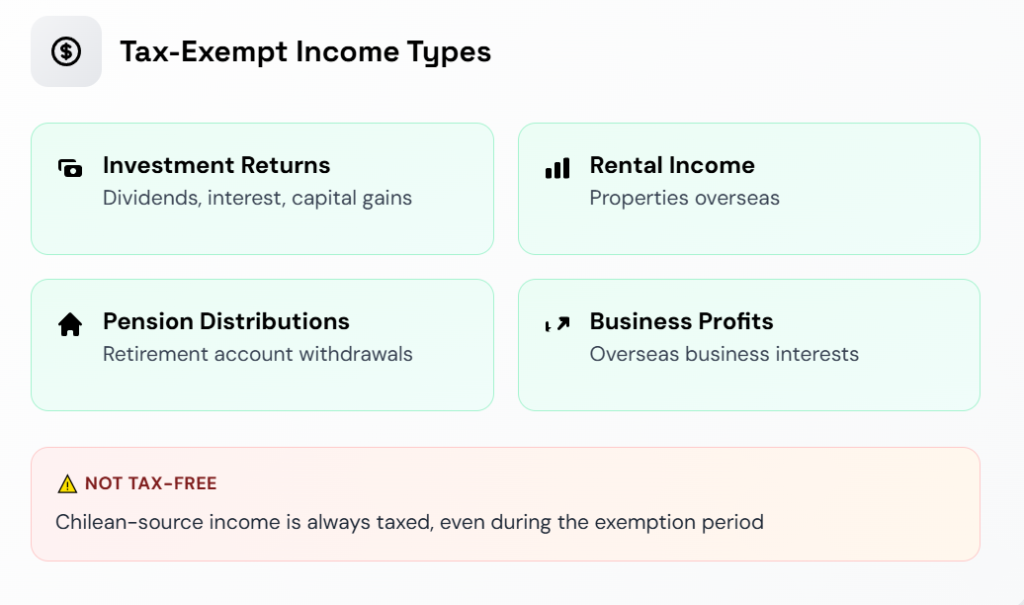

Chile generously gives new residents an incredible financial gift that most countries would never even consider: a massive three-year tax holiday strictly on foreign income. Do you receive lucrative foreign dividends directly from your brokerage account? They are absolutely not taxed by Chile.

Do you collect steady rental income from a property in Florida or Toronto, or harvest capital gains from selling overseas investments? Chile legally ignores all of it for a full 36 months. Valuable extensions for an additional three years are highly possible, easily allowing up to six total years of completely tax-free foreign income.

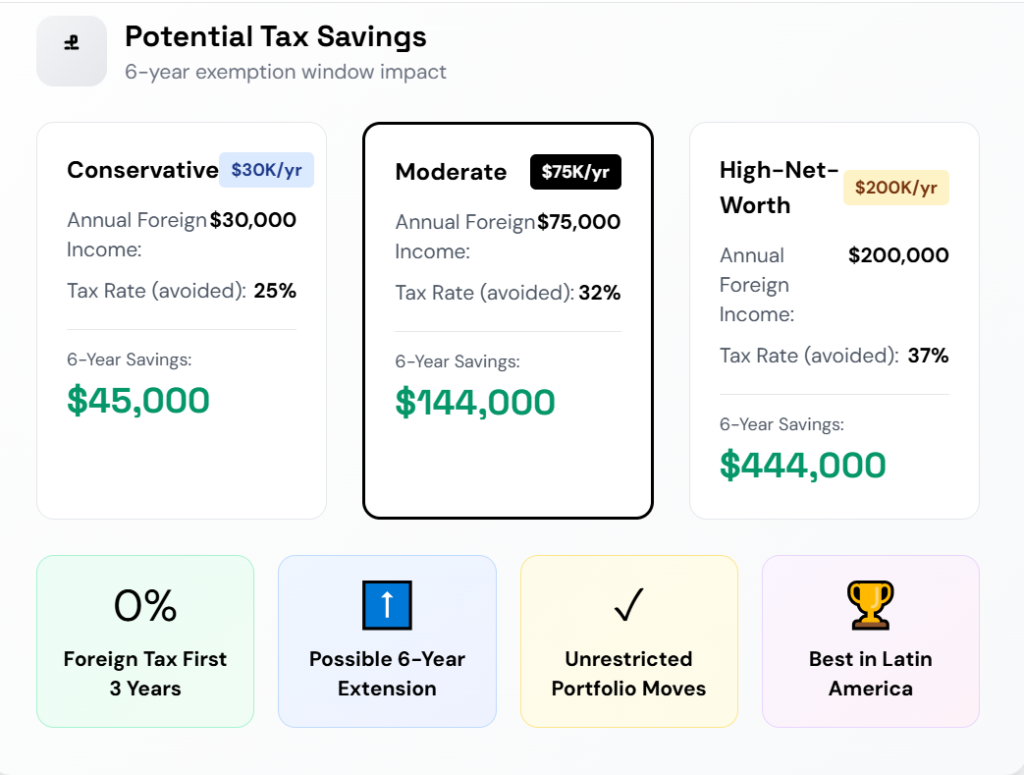

You can strategically use this golden opportunity to sell appreciated assets and realize massive gains, profitably liquidate a rental property back home, or efficiently rebalance retirement accounts and harvest stock profits. All of this financial restructuring is accomplished entirely tax-free. For wealthy retirees with substantial foreign assets, this unprecedented grace period is easily worth tens of thousands of dollars in deferred or completely avoided taxes.

Compare this immense freedom to moving to Spain or France, where punishing worldwide taxation starts the exact day you officially become a resident.

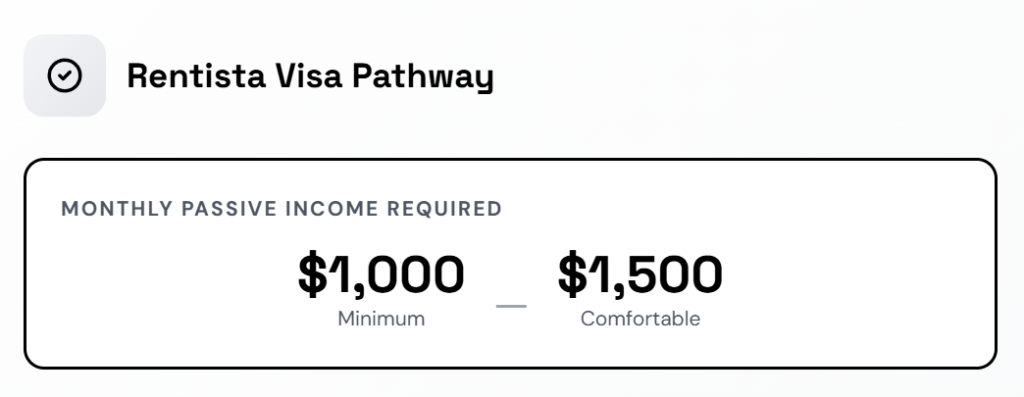

Alternatively, closely look at Portugal’s famous Non-Habitual Resident regime, which certainly offers tax benefits but notoriously phases out and carries highly complex qualification rules. The highly accessible Chilean Rentista Visa pairs beautifully with this incredibly generous tax treatment. You easily qualify with provable passive income generally sitting between $1,000 and $1,500 per month.

Standard pensions, regular Social Security checks, corporate dividends, and real estate rental income all perfectly count toward this low requirement. You are not legally required to work in Chile, but the visa generously grants a full work permit if you ever want it. After successfully completing the initial 12-month temporary permit, you can apply for permanent residency provided you physically spend at least 185 days in the country.

The glorious tax holiday is naturally not permanent, but it gives you precious time to adapt, meticulously plan, and save a considerable sum of money while doing so. For exhausted expats fleeing high-tax countries like Canada, this represents a massive, life-changing chance to save money.

Combined seamlessly with strong fiscal discipline and a resilient pension system, Chile undeniably offers a tax environment that deeply respects capital preservation. However, preserving capital means absolutely nothing if one catastrophic medical emergency instantly wipes out your entire life savings, right?

The Healthcare Advantage

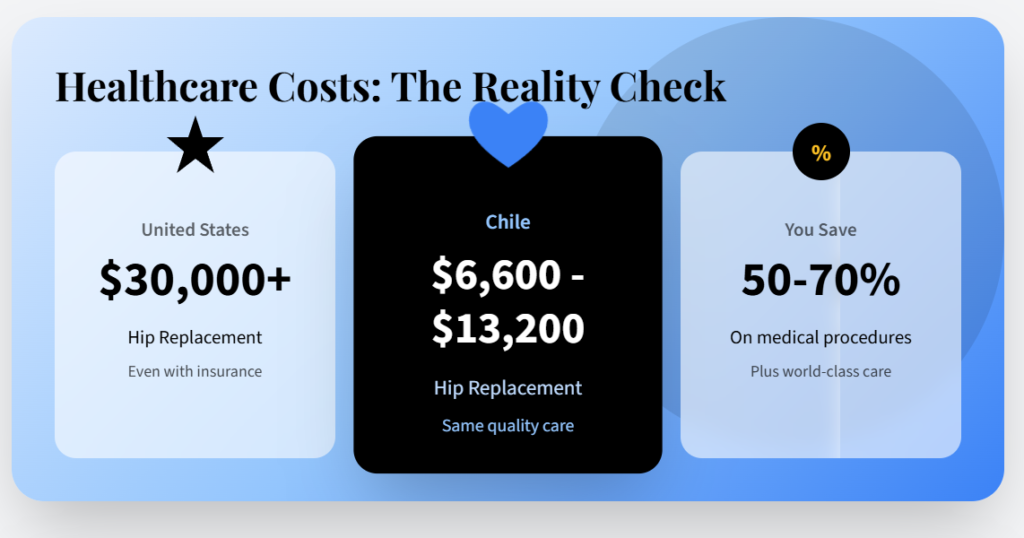

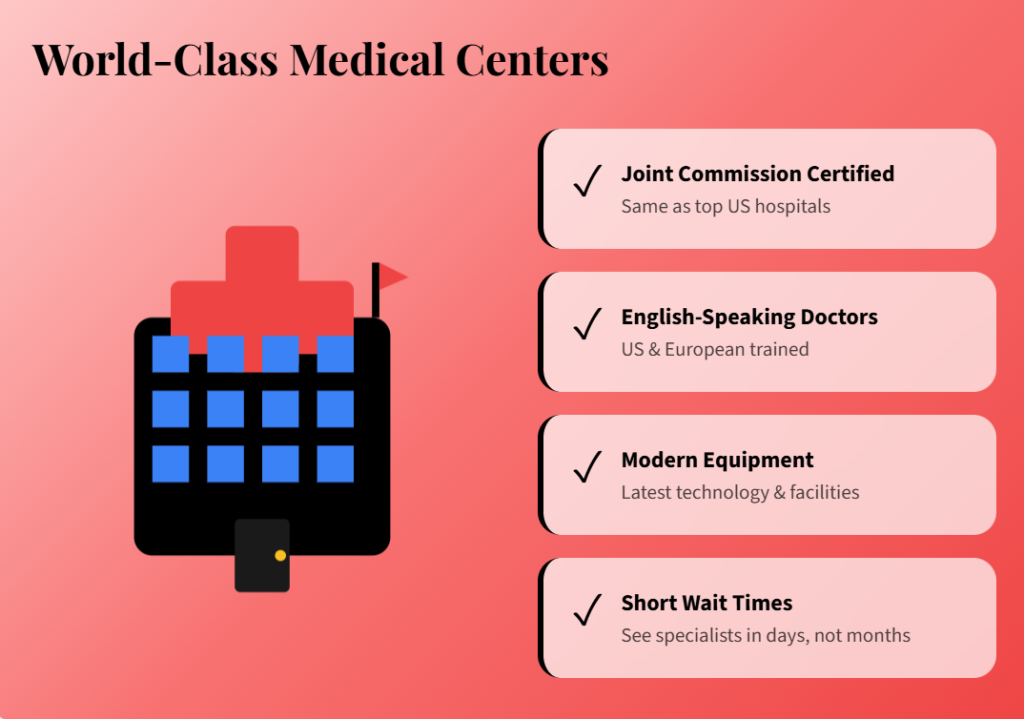

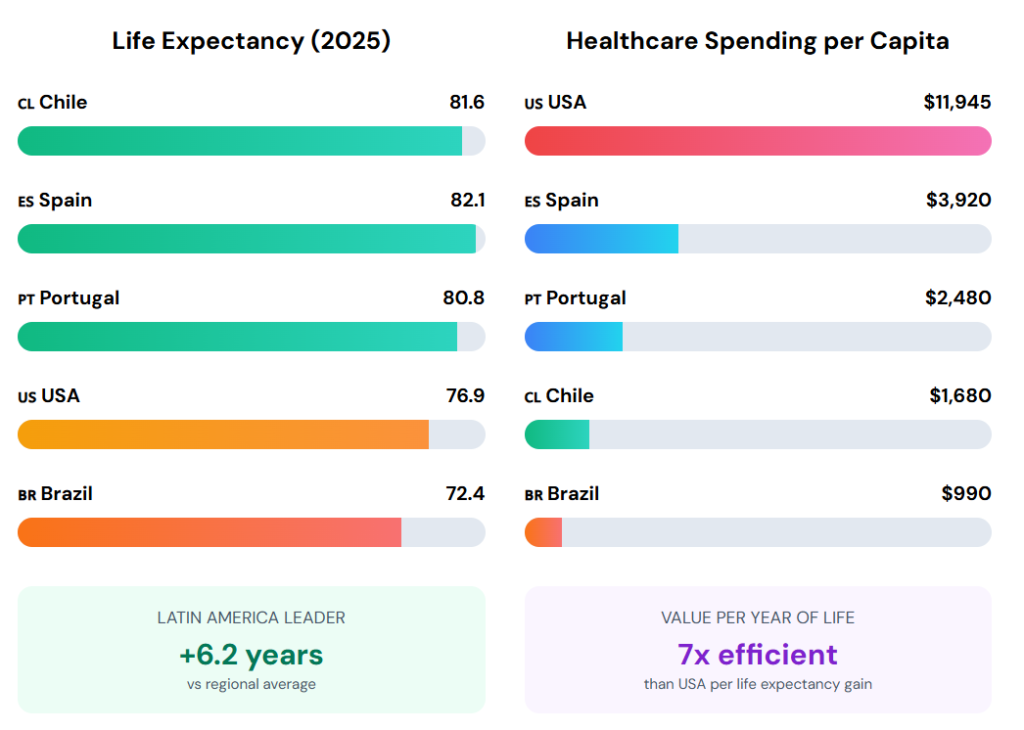

Chilean private healthcare confidently outranks both the U.S. and Canada on crucial cost-benefit metrics. That bold claim sounds completely unbelievable until you finally see the hard numbers. Clínica Alemana de Santiago and Clínica Las Condes operate at medical levels entirely comparable to top-tier U.S. hospitals.

Both prestigious institutions proudly hold Joint Commission International accreditation, which is the exact same stringent quality benchmark used to certify leading American medical centers. They feature highly modern equipment, elite English-speaking doctors who trained in the U.S. or Europe, and phenomenally short wait times. And still, the total price is usually 50% to 70% lower than what you must pay in North America.

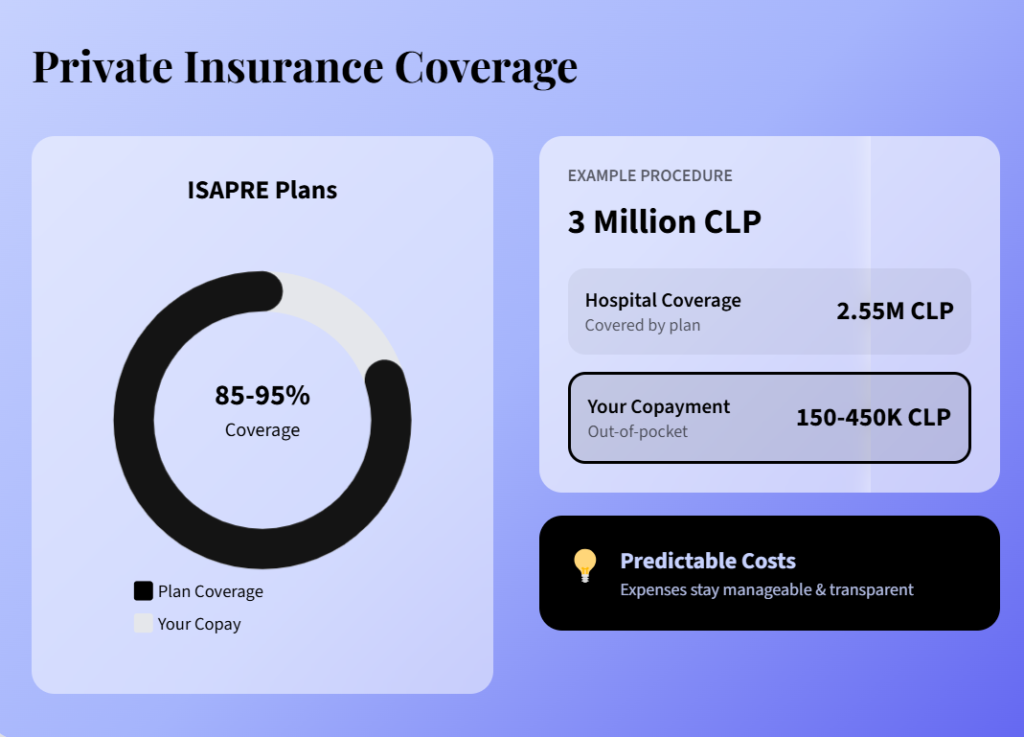

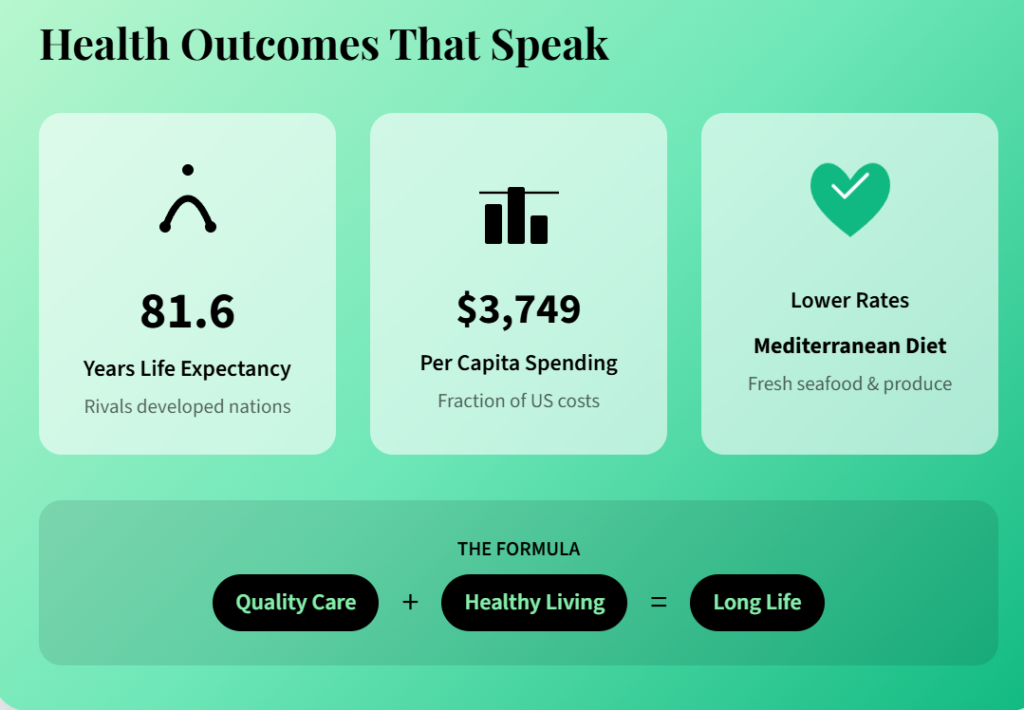

Chile surprisingly spends about $3,800 per capita on healthcare, falling far below massive U.S. levels, yet it remarkably achieves a high life expectancy of around 81.6 years. The elite private ISAPRE system, predominantly used by higher earners and expats, regularly offers 85% to 95% coverage on premium health plans. A complex medical procedure costing 3 million Chilean pesos results in incredibly minor copayments of only 150,000 to 450,000 pesos.

A full hip replacement in Chile’s highly efficient private system runs roughly $6,600 to $13,200.

In the U.S., the exact same orthopedic procedure severely costs $30,000 or more entirely out-of-pocket, even if you hold good insurance. The overarching medical system is not perfect, as the public healthcare sector seriously lags behind, but expats utilizing private insurance comfortably access care that heavily rivals or exceeds what they enjoyed in North America. For older retirees, this fundamental security is truly existential.

Private healthcare is unquestionably the largest unpredictable expense you will face in retirement. A single serious illness in the U.S. can ruthlessly drain your entire life savings in a matter of weeks. In Chile, that exact same severe illness remains a completely financially manageable event.

Private ISAPRE insurance premiums have certainly increased recently, but they remain highly affordable when compared directly to the broken U.S. insurance market. If your biggest nightmare is a bankrupting U.S. medical bill, Chile ensures you get rapid access to world-class private clinics without the sheer financial terror that defines American healthcare. Furthermore, the next major pro shows that Chile safely protects much more than just your physical health.

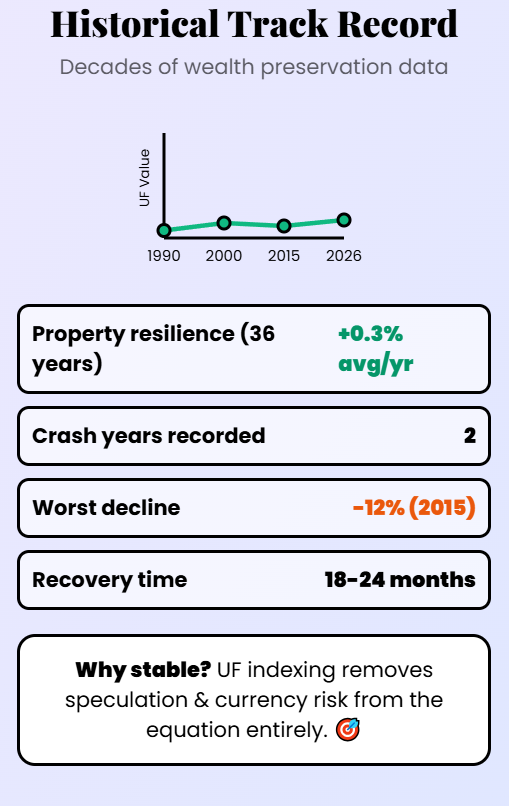

Real Estate Stickiness and Capital Preservation

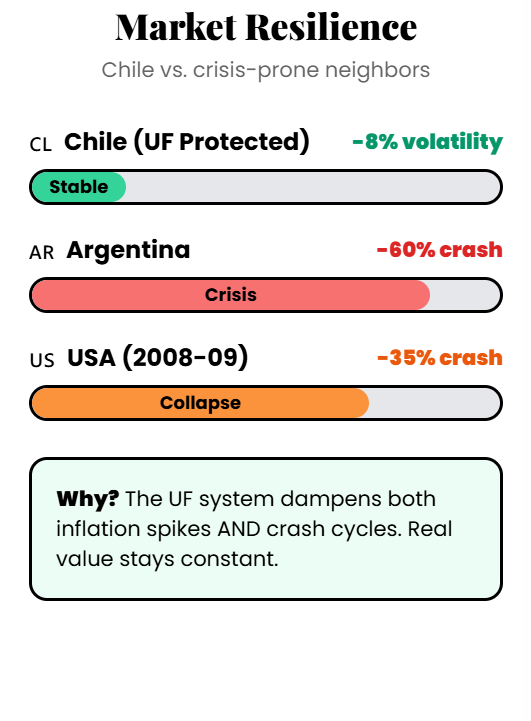

Chilean real estate essentially does not crash very often. The primary reason is an ingenious financial unit that most expats have never even heard of: the UF. The Unidad de Fomento is a highly secure daily-indexed unit that is strictly tied to national inflation.

Property prices and residential rents are fiercely denominated in UF, not in easily devalued Chilean pesos. When inflation naturally rises, the precise value of the UF rises exactly with it. In early 2026, one single UF safely equals approximately 40,000 CLP.

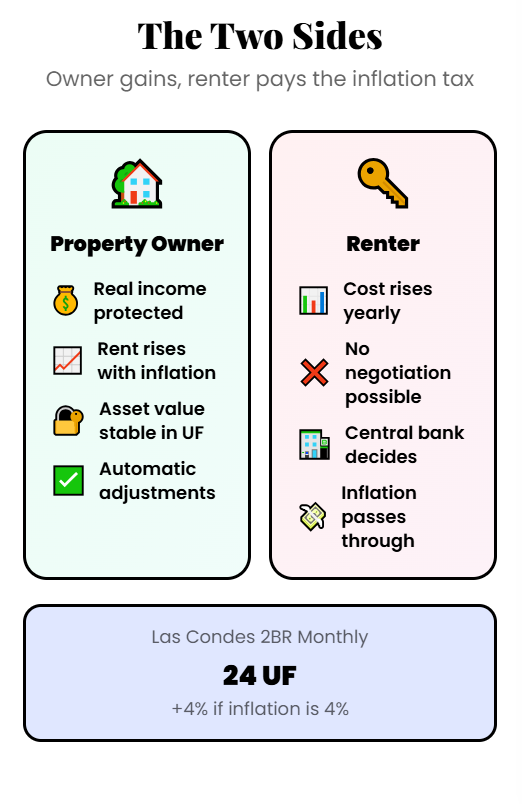

Smart landlords permanently maintain their real income because rent automatically adjusts with inflation, and property values stay remarkably stable in UF terms even when the local peso wildly fluctuates. Premium residential neighborhoods like Vitacura and Las Condes showcase incredibly sticky property values over decades. A nice home that cost exactly 4,000 UF in 2005 still comfortably trades right around 4,000 UF today in 2026.

For real estate buyers, your deployed capital is heavily insulated from sudden currency devaluation.

The physical asset successfully holds its true real value regardless of what negatively happens to the Chilean peso against the mighty dollar or the euro. On the somewhat negative side, if you are a renter, your monthly rent rises directly with inflation automatically and undeniably. Imagine signing for an apartment in Las Condes that costs exactly 30 UF per month, keeping in mind one UF currently sits around 39,700 pesos.

If annual inflation hits exactly 4%, a UF will seamlessly change to 41,300 pesos, and your rent smoothly rises 4% in peso terms. For savvy property owners, the UF acts as an absolute masterclass wealth preservation tool. Your tangible asset holds its real economic value, and your vital rental income effortlessly keeps perfect pace with the rising cost of living.

The brilliant system rigorously protects you from the quiet financial erosion that utterly destroys landlords in high-inflation environments. Compare this extreme stability to Argentina, where prime real estate prices violently collapse in dollar terms during frequent, chaotic currency crises. Alternatively, look at the turbulent U.S., where local housing markets disastrously dropped by an eye-watering 30% to 40% in 2008 and 2009.

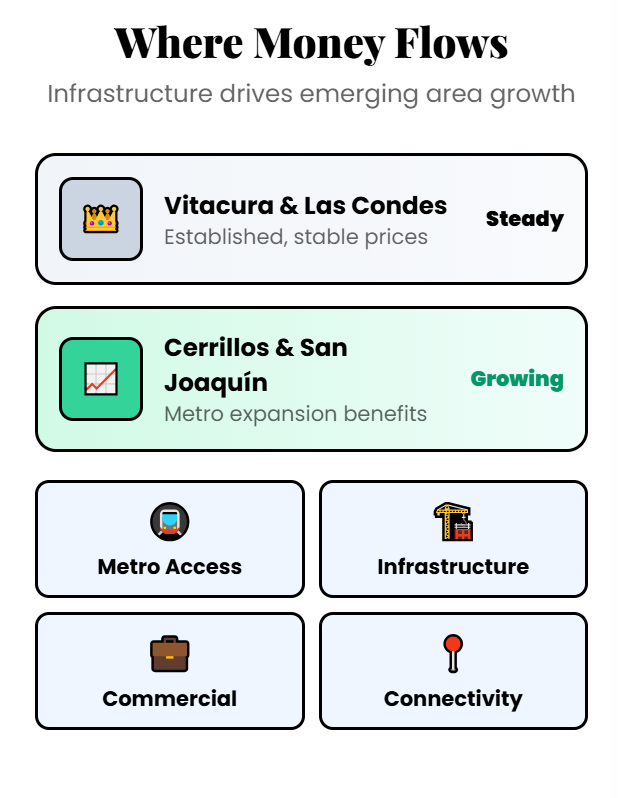

In bustling Santiago, rapidly emerging neighborhoods like Cerrillos and San Joaquín are heavily outperforming traditional luxury enclaves in terms of price increases due to massive, highly successful Metro expansions. Smart investment capital flows intensely into strategic areas benefiting directly from vital infrastructure expansion and the increasing, reliable reach of modern public transport. The wider Chilean real estate market successfully entered a slow, steady recovery phase in 2026 as punishing mortgage rates finally eased.

The ubiquitous UF effortlessly ensures that all property pricing stays entirely rational year after year. It perfectly locks in real intrinsic value and fiercely protects investors against any unexpected inflation spikes. For cautious expats heavily prioritizing long-term capital preservation and rock-solid stability, Chilean real estate offers an exceptionally rare combination of high liquidity and supreme safety.

You can seamlessly sell your property whenever you need to, as the local market functions properly and highly willing buyers consistently exist.

The Mediterranean Multiplier: Climate and Longevity

Chile stands as the absolute only Latin American country blessed with a genuinely true Mediterranean climate. The beautiful Central Chile region perfectly mirrors the stunning coastal California landscape or the sunny charm of southern Spain. You delightfully experience mild, pleasantly dry summers seamlessly followed by cool, wet winters.

There is minimal, entirely manageable humidity, allowing for incredibly comfortable year-round outdoor activity. I often enthusiastically say that the glorious Mediterranean climate is absolutely perfect both for growing world-class wine and for fostering human life. As a passionate wine lover myself, I certainly do not see that magical connection as a mere coincidence.

The globally famous Mediterranean diet absolutely thrives flawlessly in this specific coastal climate. Locals continuously consume abundant rich olive oil, fresh oceanic fish, and exceptionally good wine. In my honest professional opinion, fantastic Chilean red wine from rich varietals like Cabernet Sauvignon or Syrah confidently sits on the exact same elite level as the absolute best European counterparts.

Extensive global research consistently links this exact healthy dietary pattern to a significantly lower prevalence of dangerous obesity and deadly metabolic syndrome.

The remarkably pure food that naturally extends human life is often the exact same food that costs less and tastes significantly better. Once considered a massive, highly dangerous issue in Chile, particularly in smoggy Santiago, air quality has improved dramatically over the last few progressive years. The bustling Metropolitan Region proudly recorded its third-best air quality year since 1997 in 2025, heavily driven by brilliantly electrified public transport and highly strict bans on polluting wood-burning heaters.

Central Chile’s perfect moderate climate beautifully supports daily vigorous outdoor exercise, high social engagement, and absolutely vital stress reduction. All of these fantastic lifestyle factors actively compound to seamlessly extend your healthy human lifespan. Compare this paradise to the oppressive, sticky heat and humidity of Southeast Asia, the harsh, freezing winters of Eastern Europe, or the thick, toxic pollution plaguing many Asian megacities.

The glorious Mediterranean weather, the significantly better quality food, and the highly active outdoor lifestyle compound directly into many years of additional healthy life. The extraordinarily high national life expectancy clearly and directly reflects this wonderful reality. Chile amazingly outperforms every single country in South America and heavily rivals many elite Western European nations despite much lower healthcare spending, and the beautiful climate is undeniably one of the main reasons.

The Verdict

In Chile, you actively accept slightly higher living costs than most of Latin America, alongside a challenging, rapid Spanish accent that might be very complicated at first. In exchange, you get a highly lucrative three-year tax holiday that brilliantly lets you perfectly restructure your existing wealth without facing any financial penalty.

You also gain guaranteed access to world-class private healthcare at a mere fraction of U.S. costs, seamlessly combined with a stunning Mediterranean climate that famously pushes national life expectancy up to 81.6 years.

However, if you want to live like an absolute king on just $1,000 a month, you should definitely look elsewhere. For example, you can check out the four specific countries that I meticulously selected where you can easily have a fantastic life on exactly $1,000 per month!

Levi Borba is the founder of expatriateconsultancy.com, creator of the channel The Expat, and best-selling author. You can find him on X here. Some of the links above might be affiliated links, meaning the author earns a small commission if you make a purchase.